Man, we’re only 24 hours into the 2021 offseason and rumors are already flying around that Russell Wilson’s camp is upset with Seattle’s failure to provide adequate protection up-front. Despite the media frenzy, the reality is that the truth is somewhere probably in the middle. There is no doubt that Russell has dealt with some of the worst offensive lines in the league over the past decade (I don’t need to dig up the stats to prove that). Few quarterbacks, if any, would have come into the league behind those lines and survived, let alone be successful.

But at the same time, there is absolutely no doubt that a good portion of those sacks are on Russell. He often holds onto the ball too long, can get a little skittish, and tries to spin out of a tackle and often results in a big net loss. But I’m not here to assign blame in the blame pie. Everyone will have their take on that.

The reality is this, and most fans are in agreement on this: the Seahawks *have* to invest heavily in their offensive line. No more cheap ass free agent bullshit. No more “we’re protecting our cap health in future years because we want to contend long-term” bullshit. No more “we think we’re smarter than everyone else so we’re going to wait until wave 2 or 3 of free agency” bullshit. Their franchise quarterback will be 33 mid-way through the 2021 season. His prime is not coming, his prime is now. The window is now. The Super Bowl window is now. The clock is ticking.

The good news is there are some exciting — and talented — offensive linemen about to hit free agency shortly. In this piece, I’m not going to break down those names (we’ll do that on Real Hawk Talk), instead I’m going to discuss how their cap situation enables them to make several large acquisitions (should they want to).

So with that said, I wanted to put out a quick piece providing some insight into Seattle’s cap situation. I was seeing a lot of misinformation flying around and wanted to provide a little bit of clarity. At first, with a revenue loss from the whole COVID situation, a ~$181M salary cap limit leaves the Seahawks with about ~$5M in cap space. This can look intimidating. But this is where the nuance and the complexities of the NFL salary cap become important.

On the surface, the Seahawks look limited in their cap space — but the reality is that the Seahawks have several tools at their disposal to quickly open up additional cap space. So although they lack “cap space”, Seattle has the ability to open up large amounts of additional cap space very quickly. This is what we call “Cap Flexibility”.

I’m going to walk you through two cap tools that provides Seattle with significant cap flexibility:

- Extensions for key players (yes — you heard that right)

- Contract restructures

How extending key players can open up additional cap space

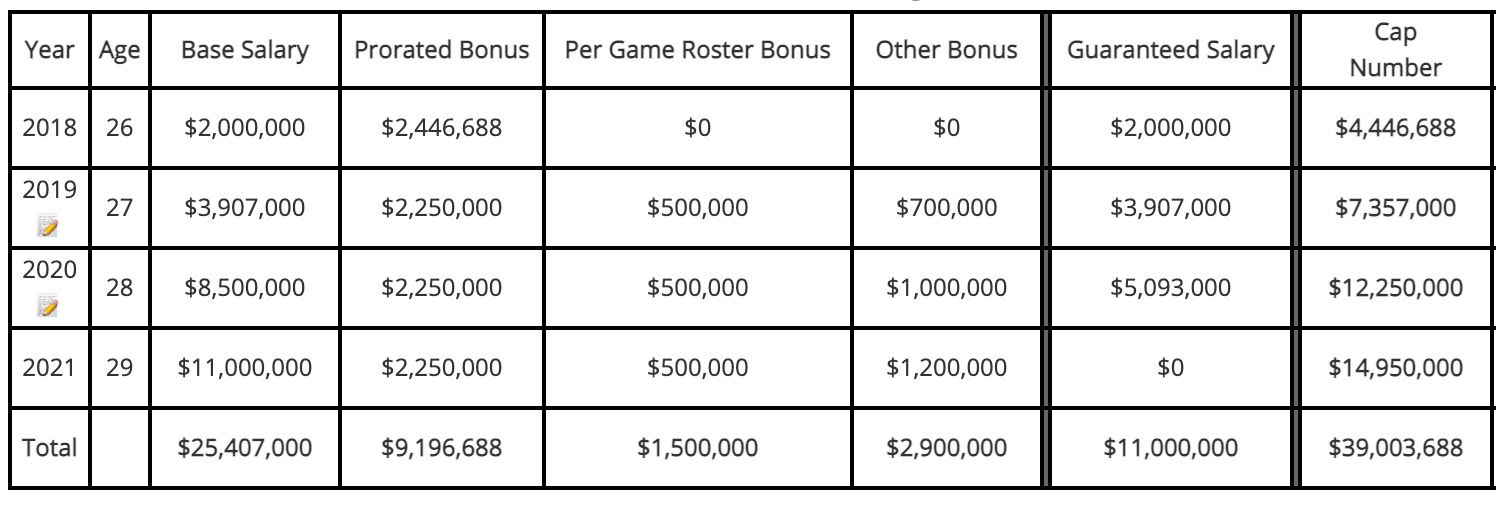

Believe it or not, extending a player can actually open up cap space — and not just a little, but a lot! The way this works can be kind of confusing, so I’m going to try and break this down as simply as possible. Let’s take Tyler Lockett’s contract for example, from Over the Cap.

As you can see above, Lockett is entering the final year of his contract extension from 2018. His 2021 cap hit is $14.95M. The base salary column — so $11M for 2020 — is paid to a player on a 1/16 per game basis ($687K per game for Tyler). The signing bonus — which is $11M but is prorated at $2.25M per year — was paid out up-front to Lockett in 2018. Now, this is critical: signing bonuses are paid out to players in a lump sum upfront, but prorated equally against the cap over the life of a contract, up to a max of five years. You might ask why he doesn’t have around $2.25M signing bonus slot for 2018 — the reason is that there was some remaining signing bonus prorated from his old rookie deal that gets accounted for (so $2.25M + old signing bonus for 2018).

So how does an extension for Lockett open up cap space? Let’s walk through this super slowly…

Tyler Lockett’s cash flow — or the money he is being paid in 2021 is $11.5M. He is getting paid $11M in base salary (paid out per game) + a $500K roster bonus that is evenly split over 16 games ($31,250 per game). The signing bonus was paid to him in 2018 — so he is not seeing that this year from a cash flow perspective.

The Seahawks would offer Lockett an extension: let’s say 4 years/$60M ($15M per year) as an example — I am making up these numbers. Let’s say that number included a $15M signing bonus and dropped his 2021 base salary to $3M. Lockett’s 2021 cash flow would go from $11.5M on his old deal to $18M in his new deal. ($15M signing bonus is paid upfront, remember?) + a $3M base salary (evenly divided over 6 games). But remember, the signing bonus is prorated over the life of the contract for cap purposes. So his new deal would drop his 2021 cap hit from $14.95M to $8.25M — opening up close to $7M in cap space.

This maneuver accomplishes three things:

- It keeps a core player with the team

- It rewards Lockett financially

- It opens up cap space for the team

This is a win, win, win. And the truth is, Lockett isn’t the only player they could work the same maneuver on. Carlos Dunlap, Jamal Adams, Quandre Diggs, and Duane Brown are all key players in need of extensions (and players I hope/assume they want to keep long term). Now I know the immediate question is “how much cap space could Seattle open up by extending these players” — well, it’s hard to precisely predict because obviously contract negotiations are unique to every single player. But I would guess a minimum of ~$20-30M if they extended all of these players. Maybe more.

Contract Restructures

This is definitely the less sexy option of the two. I’m generally not in favor of doing this, and Seattle is too. I believe they did it once with Doug Baldwin and maybe once with Russell. It leverages some of the same cash flow principles as above but is a credit-card-like-move. If they do this, they will pay for it in future years. And to be clear, that’s not an argument as to why they shouldn’t do it. It’s just the reality of it. There’s a strong argument, with the ticking window of Russell’s prime, that they should do this.

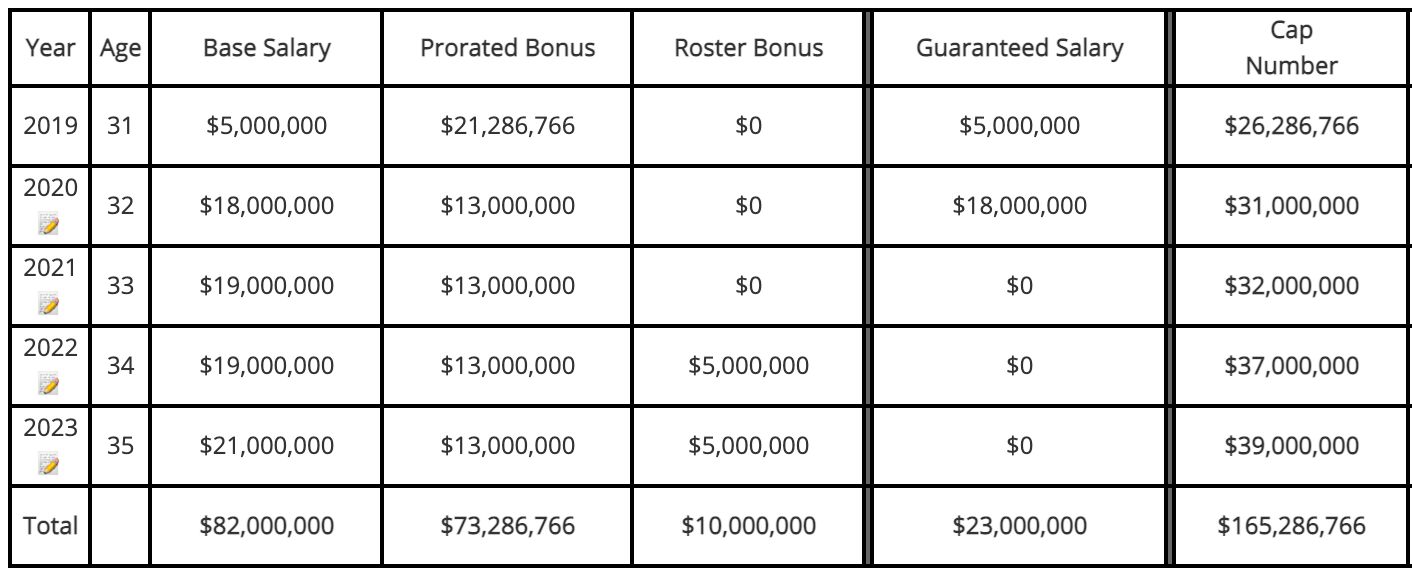

We’ll use Russell Wilson’s contract as an easy example.

His extension with the Seahawks in 2019 included a $65M signing bonus, prorated evenly against the cap at $13M per year over the life of the contract. He earns a 2021 base salary of $19M.

If Seattle wanted to, they could drop his 2021 base salary of $19M significantly and convert it to a signing bonus. This is good for the player, as it immediately puts $19M into his pocket — it’s 100% guaranteed money. Let’s say they dropped his base salary from $19M to $4M and gave him a $15M signing bonus. That $15M signing bonus would apply $5M to his cap hit for his contract years in 2021-2023. It would immediately open up $10M in cap space for the Seahawks.

So what’s the point of all of this? I guess I just wanted to shed a bit of a deeper light on Seattle’s cap situation. Although their cap health looks daunting with only ~$5M in space, they possess a deep amount of cap flexibility to aid pretty much any acquisition or move they’d want to make. If investing in the offensive line is a priority of their’s (and it better fucking be), then they have the financial ammo & capability to do it. There are no excuses anymore. Being cheap to support “sustained success” in future years is no longer a priority. Russell Wilson won’t be around forever. The clock is ticking. The time is now.